Second-quarter earnings reports have been strong in aggregate. S&P 500 revenues and earnings have grown at a healthy level quarter-to-date while beating expectations, and yet the S&P 500 neared a correction last week. Other domestic and international equity indices have already experienced corrections. The Nikkei crashed after Japan’s Central Bank raised short-term interest rates.

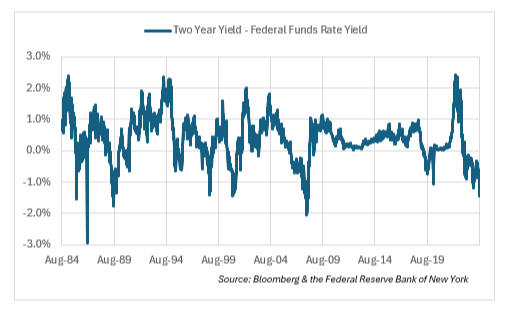

While quarterly reports have been strong, economic data is decelerating. Weaker than expected U.S. payroll reports created fears that the Federal Reserve is behind the curve again. The weekly unemployment reports and the monthly payroll report released on August 2nd point to a labor market that is growing, but one where the rate of growth has slowed materially. This has happened while inflation measures have come down and are nearing the two percent target. Core PCE is the Federal Reserve’s preferred measure of inflation. It is now around 2.6% on a year-over-year basis and trending lower. The real Federal Funds Rate, which measures the Federal Funds rate less inflation, is now close to 2.7% which is a high level historically (see chart).

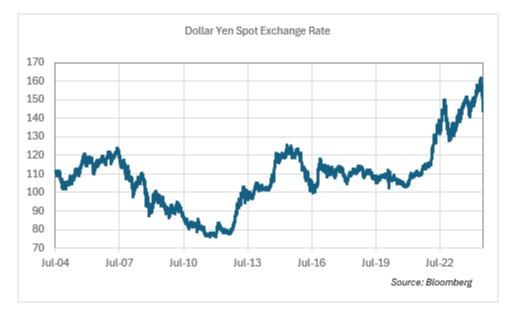

Right before payroll reports came in weaker than expected, the Bank of Japan raised its unsecured overnight call rate from 0.10% to 0.25% on July 31st. Japan has waited too long to raise rates after decades of keeping interest rates artificially low. The rate hike, while probably warranted, surprised market participants. A rapid appreciation in the yen and an unwind of carry trades where investors and market participants borrow in yen occurred (see chart). This contributed to a stock market selloff globally, and a market crash in Japan.

The drop in bond yields lends support to equities if a recession does not ensue. There are certain indicators that are concerning, but some of those indicators have been worrisome for a while. The current economic cycle is unlike any one we have seen in recent economic history and those indicators may not be relevant in 2024. Most of the data points to a decelerating but growing economy. Assuming the market avoids a recession, lower interest rates make stocks more attractive compared to fixed income and should provide support for equities later in the year.

NPP believes that the market correction is overdue and is not a reason to make drastic changes in anticipation of a protracted bear market. In any given year, a ten percent correction is more likely to occur than not. August and September are historically two of the weakest months and October usually is the best time to buy. Just last year, the market made an interim closing high on July 31st before it corrected about ten percent, only to rally in the seasonally favorable fourth quarter to finish the year above its July 31st high. Valuations were stretched before this pullback began, but now the S&P 500 seems reasonable, especially if earnings continue to grow. There is probably more time needed before this correction ends, and maybe more downside. Nevertheless, patient investors with a little bit of cash will probably be well served putting money back into equities here.