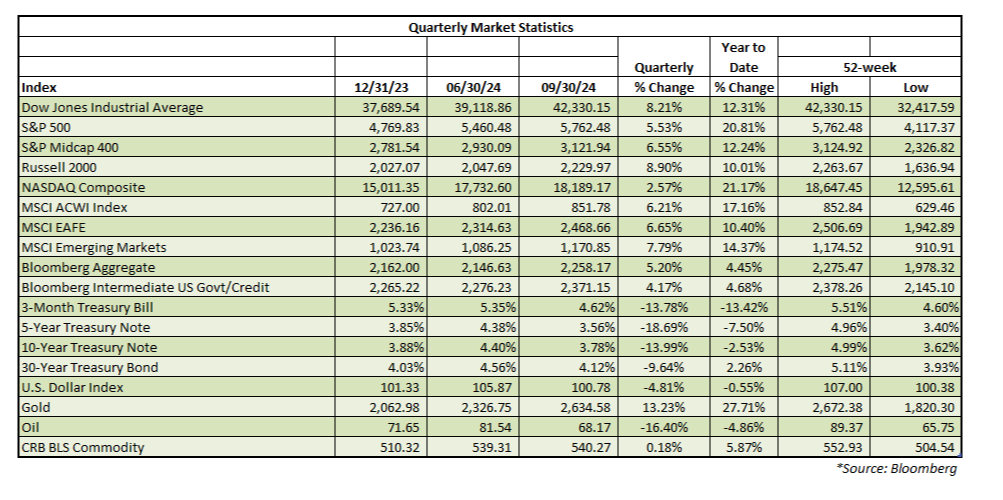

The S&P 500 turned in another strong quarter, rising 5.53% and is now up 20.81% through September 30. However, most other major indices outperformed it in the third quarter placating those that had worried about a rally concentrated in AI plays and big tech. The S&P Midcap 400 and the Russell 2000 rose 6.55% and 8.90%, respectively in the third quarter. Overseas, the MSCI EAFE Index and MSCI Emerging Markets Index modestly outperformed the S&P 500 last quarter. They were helped by declining U.S. interest rates and a falling dollar as overseas markets which generally have lower valuations started to look comparatively better.

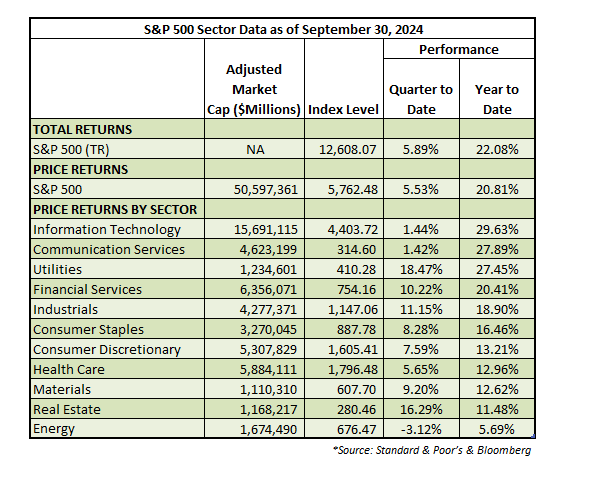

The S&P 500 was led by interest rate-sensitive sectors in the third quarter. The utilities, real estate, industrial, and financial services sectors all finished up more than ten percent. Ten of the eleven sectors rose for the quarter. The energy sector fell because of concerns over the fundamentals of the oil markets. The only other sectors to materially lag the S&P 500 were the information technology and communication services sectors. These two sectors make up more than forty percent of the S&P 500 market capitalization, and barely budged in the third quarter. The rest of the index pushed it higher, illustrating the broadening out of performance.

Treasury yields fell materially during the quarter. Rates had risen along every part of the yield curve other than the short end in the first half of the year, but falling inflation reports and less tight employment reports sent interest rates falling in the third quarter. The yield on T-Bills and five and ten-year Treasury Notes are below where they started the year. The thirty-year Treasury Bond is now slightly above its 2023 year-end level of 4.03%. The decline in yields led to strong returns for bonds. The Bloomberg Aggregate ended up 5.20% year-to-date after falling 0.71% in the first half of the year.

Gold continued to be a star performer. The precious metal rose 13.23% in the third quarter and is now up 27.71% year-to-date. Whether this is due to a weaker dollar, declining interest rates, geopolitical uncertainty or other factors, gold continues to retain a key place in client portfolios. Despite the geopolitical uncertainty, oil dropped significantly in the third quarter, falling 16.40%. Weaker economic growth overseas, and few hints of a supply/demand imbalance helped to push oil prices lower. Commodities, on the other hand, barely budged with the CRB BLS Commodity Index up 0.18% in the quarter.

Stock Performance Broadens

Equities rose in the quarter but there was some mid-quarter turbulence. The first week of August saw the S&P 500 drop from its July 31st closing price of 5,522.30 to 5,186.33 on August 5th, a decline of 6.08%. This proved to be the end of an 8.49% decline that began in mid-July and marked the low point for the quarter. The final leg of the decline was driven by a couple of ill-received earnings reports from market leaders and July payroll data that temporarily stoked recession fears. The bad news proved to be ephemeral. By the time the quarter ended, recession fears had largely passed. Lower interest rates, solid earnings growth, better inflation data, and reduced recession fears became powerful market tailwinds. If there were any lingering doubts, it certainly did not show up in the performance of the average stock. The S&P 500 Equal Weighted Index jumped 9.09% in the quarter, outperforming the S&P 500 Total Return Index which rose 5.89%. Stocks went up despite the underperformance of the information technology and communication services sectors. These two sectors have been among the market leaders and constitute about forty percent of the S&P 500 at quarter end.

It is not a time to get complacent. Corporate profits growth has improved, but earnings have not kept up with price appreciation. Market multiples have risen, and valuations give us a little bit of pause. However, earnings growth is starting to accelerate, and the dollar has weakened which should help multinationals moving forward. A resilient economy makes it tough for us to turn bearish long-term on stocks.

Bond Yields Follow Inflation Lower

Treasury yields moved lower during the third quarter. Hotter-than-expected inflation reports pushed yields higher early in the year. Since then, reports have shown inflation moving closer to the Federal Reserve’s two percent target. Rising unemployment rates increased the risk of recession, even though most investors do not expect one to occur in the next six months.

While economic growth remains solid in the United States, it has slowed elsewhere in the world. Much of Europe and Japan have seen economic growth slow or in some cases outright contract. In China, the unemployment rate in urban areas of sixteen- to twenty-four-year-olds is estimated at 21.3% according to the National Bureau of Statistics of China. It is hard to know for sure how fast or if the Chinese economy is growing, but it is much slower than we have seen in the past. As a result, inflationary pressures are abating in most of the world. This takes a lot of pressure off domestic prices and helps the Fed stay the course with this cutting cycle.

Presidential Election Looms

NPP does not know who is going to win the election. Most polls indicate a race that is too close to call, especially with five weeks to the election. Some industries that might work under one President, would likely lag under the other. However, the trade ideas also depend on if the party of the winning candidate controls Congress. There are too many tight elections and predicting which party controls the House of Representatives and/or the Senate seems likes a fool’s errand now. It would not be surprising if volatility rises due to the election, but we do not think actions are needed in client portfolios.

NPP Expects More of the Same

Equities have had a good year, and valuations have risen. On the other hand, bond yields have fallen, and this lends some support to the rise in equity multiples. The economy is still expanding, and profits are accelerating after stalling out for a bit. The broadening out in stocks is bullish, not bearish. The valuations give us pause, but they are not a reason to sell absent a recession. This is an election year. While some volatility is to be expected, we do not believe wholesale changes should be made because of it. The economic data does not support an imminent recession. Accordingly, we remain cautiously bullish on equities.